When you visit our website, information may be stored or recovered on your device, mainly in the form of cookies. We use essential cookies to ensure the website works as it should, and statistical and marketing cookies for audience measurement and content customisation purposes. We rely on Google for statistical and marketing cookies in order to measure website performance and display relevant advertising. For more information on this, please also refer to the Google policy on Business Data Responsibility.

From the Cookie Management Centre, you can set your preferences with respect to the use of cookies: accept or reject certain categories, accept all, or reject all. For detailed information on all cookies used across these three categories, please refer to our Cookie Policy.

Please note that blocking certain cookies may affect your experience and the services offered.

Essential cookies Always active

Essential cookies help the website to work as it should by enabling necessary functionalities, such as navigating between pages and accessing secure areas. These cannot be disabled in our systems.

Statistical cookies

Statistical cookies help us understand how visitors interact with our site by collecting and communicating browsing information. They make it possible to identify the most and least visited pages and to improve the overall performance of the site.

Marketing cookies

Marketing cookies are used to display relevant advertising and measure the performance of campaigns. If you choose not to allow these cookies, you will continue to see ads, but they will be less relevant to your interests.

Choose the purposes for which we may use Google products to collect and use your data:

User storage: to technically permit advertising functionality.

User data for advertising: to optimise our advertising campaigns.

Ad customisation: to tailor advertising to your interests.

Luxury under pressure: tariffs, next-gen demand, and sustainability

key takeaways.

Luxury is entering a new phase where geopolitics, trade tensions, and shifting consumer priorities are reshaping global markets, requiring brands to balance heritage with innovation

Rising US tariffs and a fragmented trade landscape are testing luxury brands’ ability to adjust pricing, supply chains, and market strategies while maintaining authenticity

Next-gen consumers are redefining luxury, prioritising experiences, authenticity, and sustainability, with front-running brands embedding purpose through systemic change rather than surface gestures

Resilience in luxury comes from strategic adaptability: companies combining craftsmanship, brand strength, and operational efficiency are best positioned to deliver long-term value amid shifting demographics and market uncertainty.

Luxury is entering a new phase, shaped as much by geopolitics as by consumer taste, building on lessons from past disruptions such as the 2008 financial crisis and the pandemic. Once buoyed by rising wealth and global mobility, the sector now faces mounting geopolitical frictions and shifting consumer priorities after a slight contraction in 2024 – a normalisation following years of expansion. As Lamborghini CEO Stephan Winkelmann notes, “We are not immune to economic fluctuations, and the current uncertainty influences our customers’ purchasing decisions.”1

Against this backdrop, US tariffs are reshaping global trade flows, brands are recalibrating growth models, and younger generations are redefining what luxury means. The result is an industry adapting on multiple fronts – commercial, cultural, and environmental.

Sign up for our newsletter

Inside the new luxury landscape: navigating US tariffs and global trade

A shifting world order has added another layer of complexity to global trade, and the luxury sector is no exception. The recent wave of US tariffs on economies worldwide illustrates how political decisions ripple through supply chains, reshaping pricing, and consumer behaviour. Emblematic luxury goods such as Swiss watches, French couture, or Italian sports cars now face the challenge of preserving authenticity while navigating an increasingly fragmented global marketplace.

The impact is uneven across economies. Japan has recorded a sixth consecutive month of export contraction1, while Switzerland’s overall exports to the US rose 43% in late 2025 driven by pharmaceuticals and gold. Yet its watch sector – with the US as its largest market – fell sharply, down 56% from August to September after stockpiling ahead of tariff enforcement.3 Earlier in the year, the Swiss State Secretariat for Economic Affairs had cautioned that punitive 39% US tariffs could weigh on 2026 growth.4 The outlook has improved following the agreement reached in November: the US will reduce its tariff rate to 15%, bringing it into line with the European Union, while Switzerland has committed to USD 200 billion of investment in the US. This adjustment lowers the expected impact of tariffs on the Swiss economy and offers a more favourable setting for export-oriented sectors. The agreement still requires formal implementation in early 2026.

Europe’s luxury and premium carmakers were among the first to brace for impact after the announcement of a 27.5% US tariff. In response, Ferrari adjusted its prices by up to 10% to reflect the new duties; Lamborghini performed similarly, prompting some buyers to pause purchases.5 German brands from Mercedes to Porsche have also warned of shrinking cash flows as tariffs erode margins – yet none can shift production to the US without compromising their “made in” identity.6 The subsequent agreement between Washington and Brussels came into effect a few weeks ago with the decrease of tariffs to 15% – another step down from the initially steep levels – with the reduction applied retroactively from 1 August.7

The UK has fared slightly better than its continental peers after securing a tariff cap of 10%. The sector has experienced notable volatility – with declines in the spring, a rebound in early summer, a setback in August, and a recovery in September8 – yet overall export values have held up more robustly than in the EU. While UK car exports rose 8.1%, exports from the EU fell 3.3%9. Even so, luxury carmakers remain wary, with Aston Martin issuing a profit warning and citing the tariff quota’s complexity.10

Amid these uneven pressures, adaptability remains the sector’s defining trait. In a world where exclusivity carries a geopolitical cost, luxury’s endurance will hinge on balancing heritage with innovation, logistics, and diplomacy.

How luxury is crafting resilience amid shifting growth dynamics

Luxury has endured multiple shocks – from financial crises and geopolitical tensions to the global pandemic – each forcing brands to reconsider how they operate.11 While heritage remains central, 2025 has shown that the sector’s capacity to adapt is what ultimately sustains it.

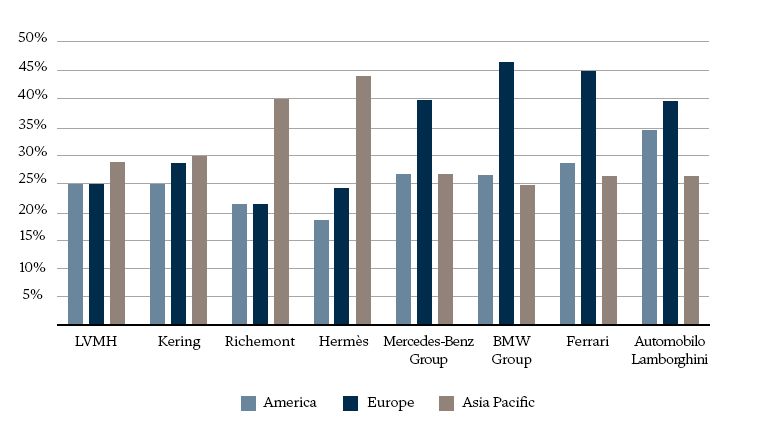

After several muted quarters, LVMH’s third-quarter results signalled a tentative turnaround, with growth returning across key markets in the US and mainland China, while Europe and Japan remained softer12. Around half of LVMH’s US sales come from products manufactured locally, providing a partial hedge against trade disruptions.13 Other Houses show similar patterns. Hermès outperformed expectations in the Americas, with a rise in sales led by jewellery, silk, and watches; Richemont’s Cartier and Van Cleef & Arpels maintained demand despite tariffs, applying calibrated price adjustments.14 Kering’s brands – Gucci, Saint Laurent, and Bottega Veneta – all saw strong North American sales15, demonstrating that loyalty to craftsmanship endures even in a challenging environment.

In the luxury and premium automotive industry, resilience takes on a different form, shaped by engineering precision and production agility. Ferrari and Lamborghini continue to record strong order books despite tariff uncertainty, while BMW expands US production to mitigate trade exposure.16 Mercedes-Benz remains cautious, particularly in China, as it recalibrates offerings to local tastes17.

This caution is well-founded. China, long a central engine of luxury growth, faced a difficult period in 2024. Mainland sales fell 1–3% early in the year as economic pressures, property sector weakness, and shifting consumer priorities weighed on discretionary spending. Outbound purchases rose as price-sensitive consumers took advantage of tax-free opportunities in Japan and Hainan.18 Yet early 2025 signs suggest a modest recovery, with some companies reporting improved demand.19

While these developments point to resilience, the path ahead is more complex than simply returning to growth, and the message is one of cautious renewal. Domestic demand in China has stabilised, but outbound consumption lags and younger consumers prioritise experiences and sustainability alongside traditional markers of luxury20. Reinvention in 2025 is not only about navigating tariffs or economic turbulence – it also involves responding to these evolving expectations, blending craftsmanship with relevance for a new generation. Luxury’s endurance has never relied solely on economic tailwinds; it is sustained by creativity, operational nimbleness, and the capacity to reinvent without compromising brand integrity.

By 2030, Gen Z and Millennials are expected to account for 60–70% of global luxury spending, while the great wealth transfer is set to pass USD 83.5 trillion to them by 2048

What’s driving luxury’s reinvention: Millennials, Gen Z, and sustainability

The luxury landscape is being reshaped by an unprecedented demographic shift. By 2030, Gen Z and Millennials are expected to account for 60–70% of global luxury spending, while the great wealth transfer is set to pass USD 83.5 trillion to them by 2048.21 Unlike their predecessors, they prioritise experiences over possessions, wellness over status, and authenticity over exclusivity. “Baby boomers, who comprise the most numerous generation in the West, are getting near the point of passing the torch. The beneficiaries of this development are people aged between 40 and 60, with mindsets, objectives, and expectations that are very different from those of the previous generation,” notes Alberica Brivio Sforza, Lombard Odier’s Managing Director in Italy.

For these next-generation high-net-worth individuals, luxury is no longer defined by ownership alone. Experiences that are immersive, culturally resonant, and socially meaningful hold far greater appeal. Leading brands are responding: Dior’s first permanent spa, housed within sister brand Belmond’s Portofino hotel, and Belmond’s own Villeggiatura luxury train journeys through Italy exemplify the blend of heritage, wellness, and cultural connection that younger consumers value.22 Across Asia and the Middle East, hyper-local experiences are taking centre stage. Louis Vuitton’s latest ship-shaped Shanghai landmark, The Louis, invites guests through two floors of exhibitions and a French-Haipai fusion café on the top deck. Meanwhile, premium carmaker Mercedes-Benz is launching China-exclusive electric vehicles with locally developed digital features.23

For these next-generation high-net-worth individuals, luxury is no longer defined by ownership alone. Experiences that are immersive, culturally resonant, and socially meaningful hold far greater appeal

This shift extends to sustainability. For Gen Z, environmental and social responsibility are inseparable from luxury. Research from Kantar shows that 69% of Gen Z luxury consumers prioritise environmental conscience, with two-thirds concerned about greenwashing.24 Leading brands are responding with systemic change rather than surface gestures. Breitling – ranked in the top 1% of companies worldwide for sustainability by EcoVadis in December 2024 – applies rigorous environmental criteria across its entire production chain, from traceable gold sourcing to transparent supply-chain reporting and carbon-offset operations.25 In the auto industry, Mercedes-Benz aims for a fully carbon-neutral fleet by 2039, embedding sustainability across its vehicles and manufacturing footprint.26 In fashion, designers such as Stella McCartney continue to explore innovative materials – including textiles designed to interact with air pollutants27 – reflecting the expanding scope of sustainable luxury.

The second-hand luxury market is also evolving as younger consumers embrace resale as part of a more responsible approach to consumption. Platforms like Vestiaire Collective have become mainstream, while brands such as Balenciaga are building proprietary programmes like Re-Sell28. The watch industry mirrors this shift: Richemont – through the acquisition of Watchfinder.co.uk29 – is tapping into a rapidly expanding second hand luxury market, with around 40% of Gen Z consumers planning to buy a pre-owned watch30.

Luxury’s reinvention is ultimately defined by its alignment with these evolving expectations. Heritage alone is no longer enough; brands must embed sustainability in an authentic way into every aspect of their offering, from product design to experiential engagement. For the next generation of luxury consumers, the ultimate status symbol is not ownership, but meaning – a portfolio of experiences crafted with purpose and respect for people and the planet.

In today’s landscape of demographic change, geopolitical pressure, and sustainability demands, enduring value lies with brands that can adapt without compromising their identity

Investing in luxury’s next chapter

The luxury sector today operates at the intersection of heritage, innovation, and shifting global dynamics. Trade pressures, demographic change, and sustainability concerns are reshaping how brands engage with consumers and preserve value. Yet the sector’s resilience demonstrates that quality, authenticity, and strategic agility endure even amid uncertainty.

Just as leading luxury houses balance craftsmanship, supply chains, and consumer expectations, we guide clients in capturing long-term value from high-quality brands. Through rigorous analysis and a long-term perspective, we help investors build resilience into portfolios.

In today’s landscape of demographic change, geopolitical pressure, and sustainability demands, enduring value lies with brands that can adapt without compromising their identity.

This is a marketing communication issued by Bank Lombard Odier & Co Ltd (hereinafter “Lombard Odier”).

It is not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a marketing communication.

share.