investment insights

Fighting fit? Germany and Switzerland, a tale of two exporters

Lombard Odier Private Bank

Key takeaways

- Both Germany and Switzerland run large trade surpluses, yet the Swiss economy has proven resilient to challenges to trade flows, while Germany, despite a weak currency, has faltered

- Germany remains obsessed with fiscal balance at the expense of much-needed infrastructure investment

- Switzerland’s exports are less price sensitive

- Much of Germany’s car market in the US, exposed to threats of tariffs, is already built by Americans

- While both economies have large fiscal cushions and need infrastructure investment, the case for doing so in Germany is more urgent

- In the short run, we remain neutral on the euro and expect the franc to remain somewhat resilient.

Germany and Switzerland’s highly export-oriented economies ranked third and fourth, respectively, in the World Economic Forum’s 2018 Competitiveness index. Both run large trade surpluses, making them the leading candidates to suffer from a less globalised world. Yet despite their apparent similarities, the German economy is struggling to grow while Switzerland has proven resilient.

The differing fortunes of the two economies are surprising. Germany’s exports benefit from the weak euro while Switzerland’s exporters contend with the strength of the franc. Germany is especially suffering from changing trade patterns following the US/China tariff dispute. Europe’s largest economy narrowly missed registering a recession last year with a -0.2% decline in the third quarter and a flat zero in the last three months of the year.

The German government forecasts that growth will slow to 0.5% this year, from an annual 1.4% in 2018. That lags the wider eurozone, which is expected to grow as much as 1.9% this year. In contrast, the Swiss economy expanded 2.5% in 2018 and is forecast to grow 1.2% this year.

Germany’s near-recession in 2018 has contributed to the European Central Bank keeping interest rates on hold this year and at least into 2020. That means there is little threat to the economy from a dramatic rise in core interest rates.

In the circumstances, it strains credibility that even the latest German budget continues to be obsessed with fiscal balance, at the expense of investment. Income tax revenues and total tax incomes in Germany have slowly grown while the country has cut its debt-to-GDP ratio to 60.9%, from 81.8% in 2010. This evolution, with low unemployment, is largely thanks to labour reforms starting in 2003 under Gerhard Schroeder.

Hergestellt in den USA

Germany’s carmakers are attracting particular attention at the moment. Germany accounted for 55% of the European Union’s car exports last year, which made up 13% or 70.2 billion euros of the country’s total exports.

As part of the Trump administration’s attempts to curb the US trade deficit, it has threatened to target German carmakers by raising import duties on EU motor vehicles and parts tenfold, to 25%, citing “national security” concerns. But while the US bought 1.34 million German cars and vans in 2018, making it Germany’s biggest auto export market, as many as 800,000 German cars are built by around 50,000 Americans, working in the US.

Apart from misjudging the reality of German cars on American roads, the Trump administration is underestimating the importance of the eurozone's economy, which represents approximately 16% of the world's GDP. The US economy might also suffer the consequences of a trade war with the European trading bloc.

Swiss challenges

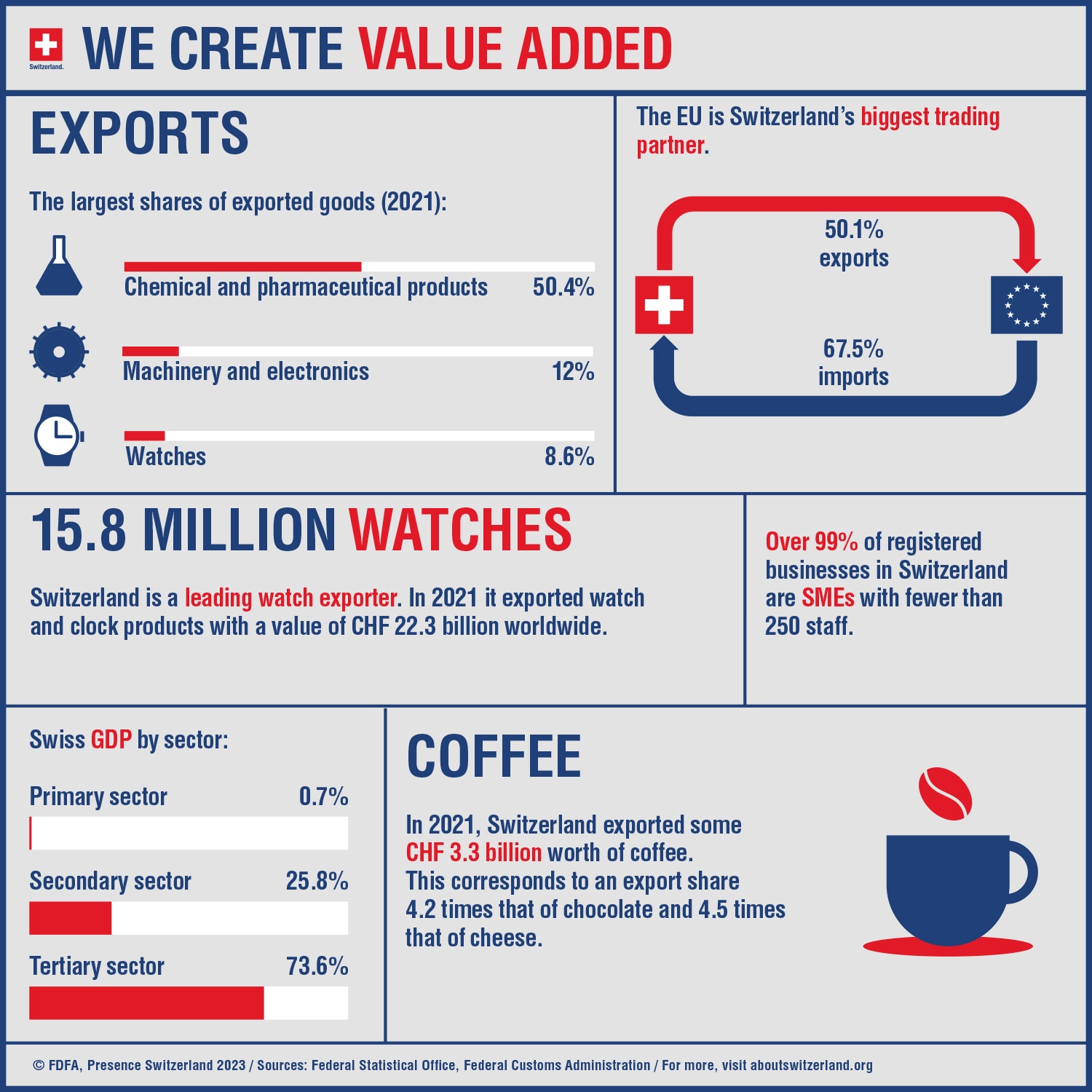

Switzerland’s economy is also highly export-dependent although more reliant on trade with the neighbouring EU, which accounts for around three-fifths of Swiss exports and more than 70% of imports.

At first glance, we would expect Switzerland’s economy to face greater challenges than Germany. The economy has the twin problem of a strong exchange rate that acts as a safe-haven currency while depending on exports in an increasingly tense global trade environment.

Switzerland’s current account surplus, which hovers around 10% of GDP, now largely consists of the trade balance, with high added-value chemical and pharmaceutical goods accounting for 45% of all exports. Swiss watch exports in 2016 accounted for 19.4 billion Swiss francs of exports, equivalent to 9.2% of exports, while the country also exported 2 billion francs of coffee. While Swiss exporters are recording slower demand and investments, companies are also taking advantage of the strong franc to source cheaper inputs and raw materials.

Fit for purpose?

In common with Germany, Switzerland has limited monetary capacity to respond to further economic shocks. Although Switzerland enjoys an independent central bank, it is restricted by its need to maintain a ceiling on its safe-haven currency. Germany on the other hand has a common monetary policy with the eurozone. This said, both economies have huge fiscal capacity to respond to negative developments.

Switzerland’s federal fiscal rule or “debt brake,” first used in 2003, reduces public debt by demanding that the national budget runs a surplus when the economy is growing, in order to sidestep the need for radical adjustments or additional debt in a downturn. Just as in Germany, Switzerland’s debt brake limits the country’s ability to invest in its own future. The difference is that in Switzerland’s case, the need to release the brake is less urgent than in Germany.

A German decision to make use of its fiscal cushion to spend would undoubtedly improve the eurozone’s economic strength, however, the first beneficiary of a smaller German trade surplus would be Germany as it effectively exports savings that would be better spent on improving domestic infrastructure, including technology.

The Swiss economy undoubtedly appears less price sensitive, given its value added export-oriented economy. Still Germany and Switzerland remain highly dependent on a globalised trading system which is being undermined by US protectionism prepared to wreck international supply chains in the interests of a misguided attempt to re-nationalise American industries.

In this environment of resurgent protectionism at the end of the 21st century’s second decade, it’s worth reminding ourselves of something that we thought a truism. Only free-moving international trade can sustain a modern economy. And any exporting nation inevitably depends on importing what it cannot produce efficiently at home.

Havens, outlook

Looking ahead over the next few months, we remain neutral on the euro, as trade tensions globally are negative for the common currency in general and Germany in particular. This said, the weaker euro also suggests that the use of the currency by investors to fund carry trades will unwind. And longer term, looking toward the end of 2019 or early next year, we expect the euro to appreciate modestly if the eurozone’s economies pick up.

Near term, the CHF may remain somewhat resilient due to risk aversion and potential flaring up of frictions between Italy and the European Commission. However, the combination of deeply negative interest rates and flat domestic inflation will create headwinds for the franc over the medium term.

Important information

This document is issued by Bank Lombard Odier & Co Ltd or an entity of the Group (hereinafter “Lombard Odier”). It is not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a document. This document was not prepared by the Financial Research Department of Lombard Odier.

Read more.

{kind=link}

share.